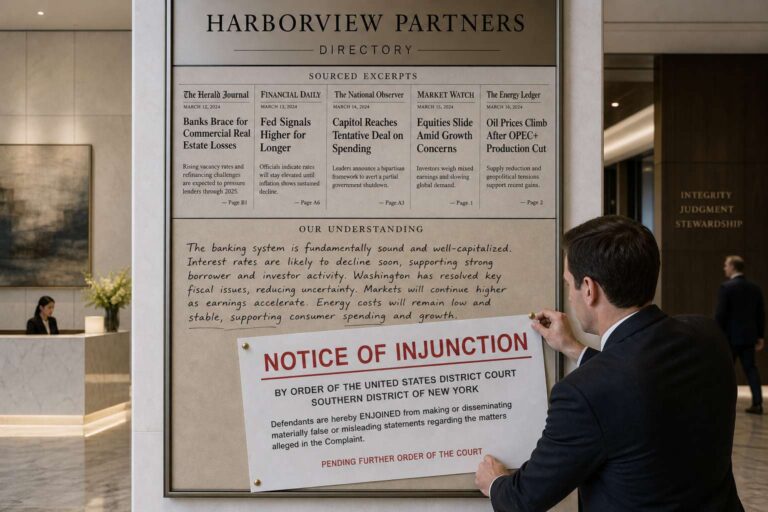

A German court issued a temporary injunction on May 28 barring Google from repeating false statements about two Munich-based publishers generated by its Artificial Intelligence Overviews feature. The case centered on outputs that falsely linked the publishers to scams, subscription traps and dubious business practices, even though those claims did not appear in the linked sources. The system had invented the connections by combining and evaluating material from multiple third-party sites.

The Regional Court of Munich treated Google’s Artificial Intelligence Overviews as Google’s own content, not as neutral pointers to third-party information or conventional search results. Google argued that search engines act as intermediaries and that users could verify summaries by checking linked sources, but the court rejected both positions. The ruling drew a distinction between relaying outside information and generating new, substantive statements that rewrite, combine and evaluate source material. Google told The Decoder on June 11 that Artificial Intelligence Overviews are designed to reflect information already available on the web, that it invests heavily in quality so most responses provide accurate information, and that it is carefully reviewing the decision, which is not yet final.

The decision is provisional and not binding in US courts, but its logic is relevant to insurers and intermediaries deploying generative Artificial Intelligence. In the United States, intermediary protections such as Section 230 of the Communications Decency Act rest on the same fault line: they protect a party that hosts or transmits someone else’s content, not one that authors its own. With no Artificial Intelligence-specific federal liability statute resolving the issue differently, disputes would fall back on defamation, negligence, consumer protection and data accuracy doctrines.

Insurance exposure is concentrated where generative systems make checkable factual claims about identifiable parties or customers and present them as finished answers. That includes customer-facing chatbots summarizing coverage, eligibility tools, claims assistants producing settlement recommendations and underwriting copilots drafting risk assessments of named businesses. Practical controls now include inventorying every generative feature that makes factual claims, separating verbatim retrieval from synthesis, grounding outputs in source material, logging source-to-statement mappings and clarifying vendor contracts before liability arises through a carrier-branded interface.